We recently discussed the importance of diligence when acquiring distressed commercial mortgage loans, providing a diligence checklist for the process. Given that any foreclosing mezzanine lender may step “into ownership” if it forecloses upon its mezzanine loan, perhaps even greater care should be exercised when considering the purchase of a distressed real estate mezzanine loan. As with a mortgage loan, diligence is key!

Before describing the diligence that should be performed prior to purchasing a distressed mezzanine loan (or, really, any mezzanine loan), let us quickly describe a mezzanine loan.

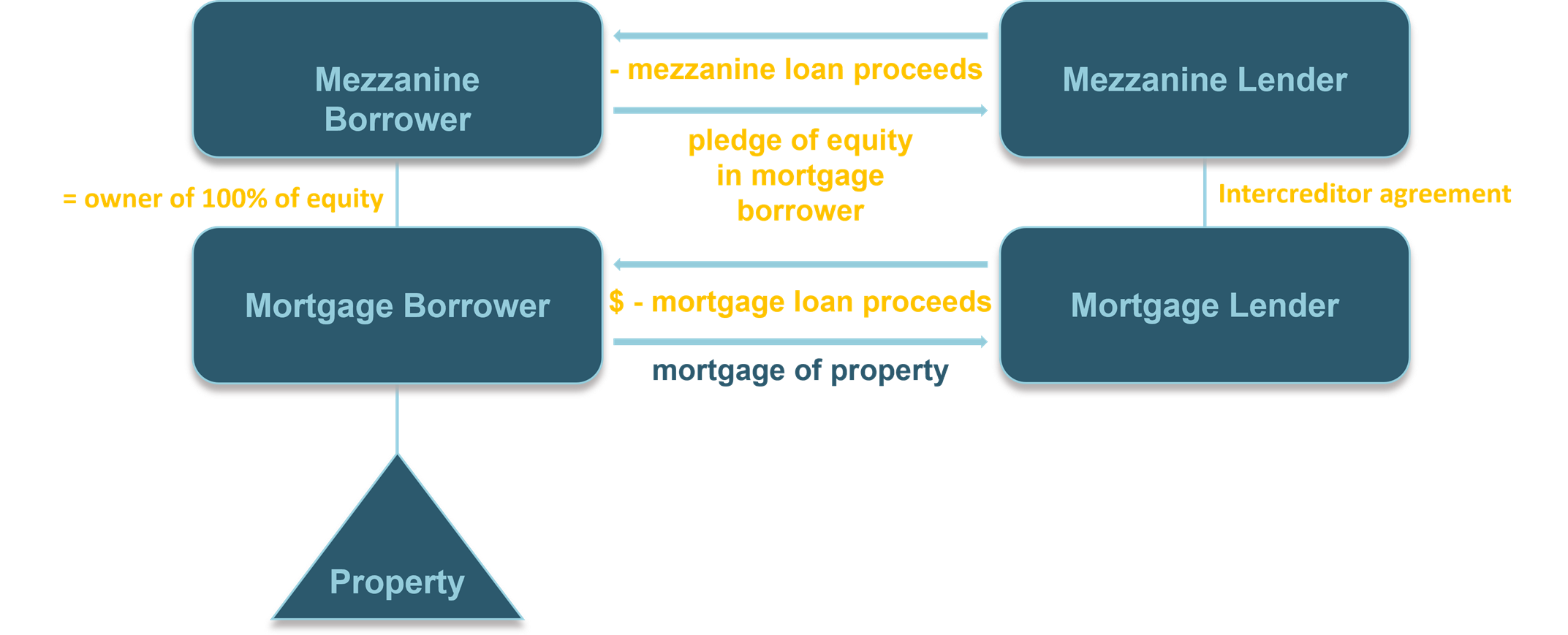

A mezzanine loan is a loan to the direct or indirect owners of a property owner.

As can be seen on the above chart, a mezzanine loan is a loan to an entity (the mezzanine borrower) that directly (or in some cases indirectly) owns the property owner. A mezzanine loan is not secured by a lien on real estate collateral. Instead, a mezzanine loan is secured by a pledge of the equity interests in the property owner. So that the mezzanine lender’s loan is worthless if the mortgage lender forecloses on its mortgage loan or accepts a deed in lieu—and such that the mezzanine loan is structurally subordinate to any mortgage loan and property level liens (such as real estate tax liens, mechanic’s liens or judgment liens).

Because the collateral for the loan comprises pledged equity interests (i.e., personal property), the Uniform Commercial Code (UCC) and not real property law applies when the mezzanine lender enforces its remedies.

We’ve described the diligence to be conducted when acquiring a distressed mortgage loan. When a potential mezzanine loan purchaser is exploring a mezzanine loan acquisition, even closer scrutiny is required since any foreclosing mezzanine lender could “step into the shoes” of the owner. Diligence is critical!

By way of illustration, in addition to the items we’ve discussed in relation to acquiring a distressed mortgage loan, any purchaser should also focus (as would any owner of the property) on the following items:

- The status of the mortgage loan, particularly any defaults. Are they curable? What is entailed to cure such defaults, and what is the cost of curing such defaults?

- Outstanding real estate and other taxes;

- Mortgage liens, and mechanic’s and judgment liens (so the state of title, generally);

- Environmental issues and liabilities, and the condition of the property;

- Income streams from the property, tenancies and obligations to tenants (such as tenant allowances and build-outs);

- Outstanding and potential liabilities under condominium documents, reciprocal easement agreements or similar documents (and are there liens for unpaid common charges or assessments?);

- Outstanding and potential liabilities under any management agreements and service contracts (and are such agreements terminable?);

- Outstanding and potential liabilities under union contracts, including unfunded pension liabilities;

- If the mezzanine lender is “behind” a construction loan, the status of construction including the status of payments to contractors, design professionals and others, defaults, the terms of the construction and design contracts, lien waivers, potential mechanic’s liens – and what is entailed to achieve completion (and when); and

- If the business operated at the property is a hotel, any management or franchise agreements (are such agreements terminable?)—and any cross-default or restrictions on transfers in such agreements.

Remember that if the mezzanine lender forecloses and itself acquires ownership of the property, it is liable for all these matters—so property level diligence is critical!

It is also critical to diligence and evaluate the terms of the Intercreditor Agreement (ICA), also shown on the chart above. The ICA is the agreement that is typically entered into by the mortgage lender and the mezzanine lender and it governs the relationship between the mortgage loan (on the one hand) and the mezzanine loan (on the other), granting to the mezzanine lender more (or less) protections.

As a preliminary matter, what does the ICA provide with respect to transfers of the mezzanine loan? Many ICA’s provide that transfers of controlling or majority interests in mezzanine loans and foreclosures (and related transfers) of mezzanine loans may only occur without rating agency approval or mortgage lender approval (if the mortgage loan has not been securitized) if they involve transfers to certain predefined “Qualified Transferees” that meet certain largely financial (and usually negotiated) “Eligibility Requirements.” So a preliminary question is: Is the buyer a “Qualified Transferee” – or will the purchase require mortgage lender (or rating agency) approval?

Note that ICAs generally restrict a lender from selling its loan to the borrower or affiliates of the borrower and contain “neutering” provisions such that a loan held by a borrower or borrower affiliate is not entitled to the many protections afforded to mezzanine lenders under the ICAs (or may not have the right to purchase the mezzanine loan at all!)

The next matter to diligence in the ICA are the cure rights granted to the mezzanine lender. Recall that the mezzanine loan is in distress and that, likely, the mortgage loan is also in “distress” or potentially in distress. In this regard, many ICA’s grant to mezzanine lenders certain rights to cure both monetary and non-monetary events of default under the mortgage loan. But does the ICA cap the number of monetary cures that may be available? What does the ICA require in connection with the cure (by the mezzanine lender) of non-monetary defaults under the mortgage loan? Is there an outside time period for such cures – and what requirements exist? What would be entailed, practically speaking?

ICA’s often also address enforcement by the mezzanine lender—and impose requirements on any such enforcement). What are these restrictions? Many ICAs require, for example, that:

- the transferee of the collateral be the mezzanine lender or a “Qualified Transferee” (or otherwise approved);

- the foreclosing mezzanine lender, or a third-party purchaser, provide “replacement guaranties and environmental indemnities” concurrently with (or within a short period of time following) the foreclosure. These replacement guaranties and indemnities typically cover actions that are taken following the date on which the foreclosure occurs—and are typically required to be delivered regardless of whether the original guarantors and indemnitors are released. But does the ICA require that all guarantees be put up by the foreclosing lender (including payment guaranties)? Or does it “tweak” the forms of existing guarantees to better “fit” the new guarantor and reflect specified guaranteed obligations?

- the property be managed by a pre-qualified or mortgage lender approved property manager—and hard cash management may be required.

Also, ICAs typically grant to the mezzanine lender the right to purchase the mortgage loan upon the occurrence of certain triggers – typically including (i) mortgage loan Events of Default or acceleration; or (ii) a securitized mortgage loan becoming a “specially serviced” loan. What is the purchase price in such event? What is the time period within which such right must be exercised? Does it lapse?

Similarly, ICAs typically grant a short standstill to mezzanine lenders prior to the mortgage lender’s accepting a deed-in-lieu. (For a more in-depth discussion of these provisions, see The Role of ICAs between Mortgage and Mezzanine Lenders and Mezzanine and Construction Loans—Considerations and ICA Provisions.)

As we’ve demonstrated, the need for diligence when acquiring any form of distressed debt is critical, but an understanding of enforcement under the Uniform Commercial Code (UCC) is also critical. So what does the purchaser of a distressed mezzanine loan potentially face? Next, we’ll take a closer look at the UCC.

This is the second in a series of posts exploring key considerations for the acquisition of distressed real estate debt. In our next installment, we’ll provide a roadmap and tips relative to enforcement under the UCC.

RELATED ARTICLES

Acquiring Distressed Commercial Mortgage Loans: A Diligence Checklist

UCC Foreclosure Basics: Acquisition of Distressed Real Estate Mezzanine Debt

Acquisition of Distressed Loans: Bankruptcy Considerations and the 363 Sale